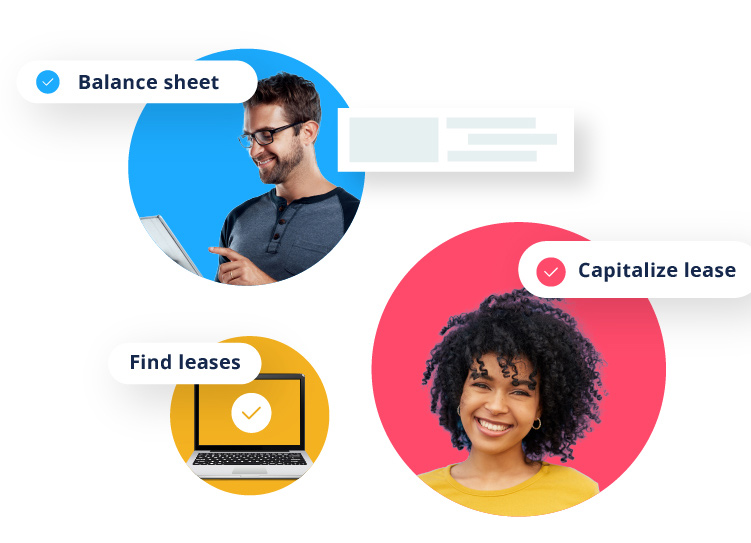

Map to General Ledger (GL) accounts. Select fiscal calendar. Set policies and controls. Use self-service bulk import to load and validate leases.

Know the lease accounting is right, with built-in classification and governance. Comply with ASC 842, IFRS 16, GASB 87, GASB 96, and all previous standards.

Choose from 15 ready-to-use reports. Use step-by-step workflows to walk through the lease accounting close. Export ERP-ready data to stay in sync.

Standard

Overview of FASB lease accounting standard

In 2019, the latest FASB standard on lease accounting, ASC 842 (ASU 2018-11), went into effect for most public companies.

Guide

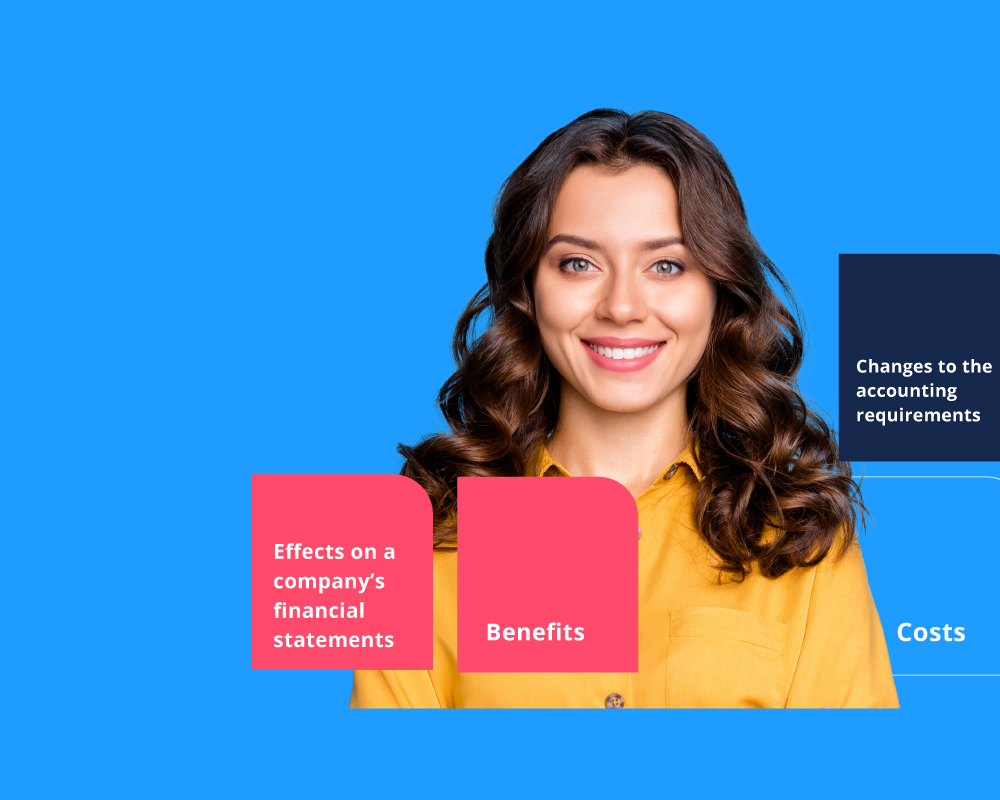

How to choose lease accounting software

Ask your software vendor these 10 questions to determine if they have what it takes to help you get and stay compliant.

Brochure

EZLease overview

The fastest, easiest way to comply with ASC 842, GASB 87, GASB 96, and IFRS 16. Guaranteed!

Standard

Optimize IFRS 16 compliance

In 2019, the latest IASB lease accounting standard, IFRS 16, began to go into effect for companies worldwide.

Standard

GASB 87 lease accounting standard

GASB 87 changed how most leases are reported by requiring them to be capitalized and recorded on the balance sheet.

Standard

GASB 96 SBITA accounting standard

Learn how to account for Subscription-Based Information Technology Arrangements (SBITAs) under GASB 96.

Overview of FASB lease accounting standard

In 2019, the latest FASB standard on lease accounting, ASC 842 (ASU 2018-11), went into effect for most public companies.

Confessions of a spreadsheet martyr

Spreadsheets may be inexpensive and easy to use, but they also overpromise and underdeliver. Find out...

ASC 842 lease accounting standard

For companies who want to achieve and maintain compliance with the lease accounting standard.

How to choose lease accounting software

Ask your software vendor these 10 questions to determine if they have what it takes to help you get and stay compliant.

Data sheet

The fastest, easiest way to comply with ASC 842, GASB 87, GASB 96, and IFRS 16. Guaranteed!

Optimize IFRS 16 compliance

In 2019, the latest IASB lease accounting standard, IFRS 16, began to go into effect for companies worldwide.

GASB 87 lease accounting standard

GASB 87 changed how most leases are reported by requiring them to be capitalized and recorded on the balance sheet.